You don’t have to look far to understand why most Indian households struggle to make ends meet despite rising incomes. It isn’t just about how much you earn. It’s about how much intention you bring to the way you spend. This is where a new-age budgeting strategy steps in — one that’s less about spreadsheets and more about behavior.

It’s called Zero-Based Budgeting (ZBB). And it’s flipping the script for millions of middle-class families across India.

What Is Zero-Based Budgeting?

The term may sound complex, but the logic is simple. With this budgeting strategy, you don’t carry forward last month’s expenses. You start fresh. From zero.

Every rupee you earn gets assigned a role—before you spend it.

Salary comes in? Good. Now tell your money what to do.

Groceries: ₹5,000.

Rent: ₹12,000.

SIP: ₹4,000.

Emergency fund: ₹2,000.

Electricity: ₹1,200.

Diwali savings: ₹500.

And so on, until every rupee has a purpose. Nothing is left “unassigned” or “left over.” You take full control.

Why Is It a Game-Changer for Indian Families?

Traditional budgeting in India usually works like this:

Income – Expenses = Savings

But that’s backward.

Zero-Based Budgeting inverts this idea:

Income – Savings & Investments = Expenses

You allocate your non-negotiables first. Investments. Emergency corpus. Insurance.

Everything else—your lifestyle choices—must fit into what’s left.

This is a budgeting strategy that forces discipline. And for middle-class families staring down rising costs, that discipline could be the edge.

How to Implement Zero-Based Budgeting (ZBB) in 2025

Let’s break it down into five steps:

1. Know Your Monthly Income

Don’t guess. Write it down. Include your full-time salary, freelance gigs, rental income, interest from FDs — whatever hits your bank account.

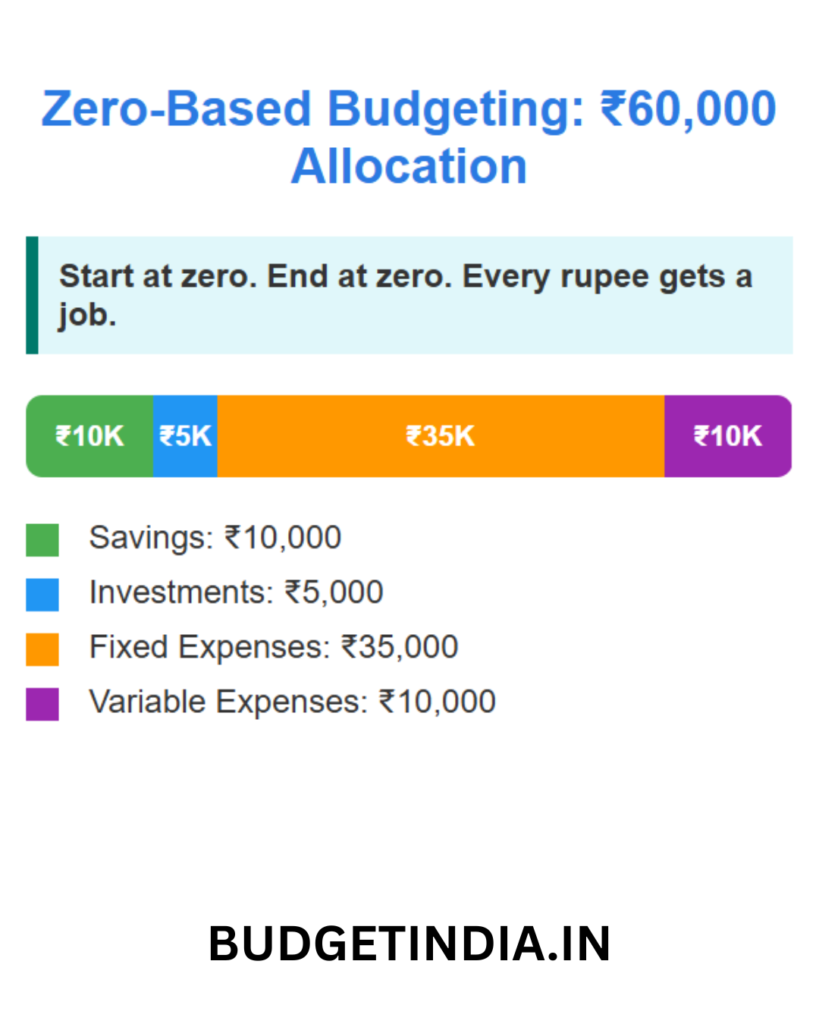

Let’s say it’s ₹60,000.

2. List All Your Expenses

Now jot down every single category you’ll spend on this month. Think beyond groceries and rent.

Add categories like:

- Health insurance premium

- Monthly SIP

- Annual festival fund

- School fees savings

- Personal treats

- Netflix subscription

Be brutally honest. Don’t leave anything out.

3. Give Every Rupee a Job

This is the cornerstone of the zero-based budgeting strategy.

You don’t say “I’ll spend what I can and save what’s left.”

You say: “Here’s what I’ll save, and I’ll spend what’s left.”

So if your savings goal is ₹10,000, investments ₹5,000, and fixed expenses ₹35,000—then your variable expenses must fit in the remaining ₹10,000.

And remember: The total must equal ₹60,000. Not ₹59,500. Not ₹62,000.

You start at zero. You end at zero. That’s the rule.

4. Track & Adjust

Life won’t always play along.

One month your electricity bill will spike. Another month your child’s school project might cost more than expected.

This is where you don’t panic—you pivot.

Pull money from a “less urgent” category. Maybe skip a weekend dinner out and cover the gap. That’s the beauty of ZBB. You control the levers.

5. Evaluate Monthly

Each month is a fresh start. Not a continuation.

So you sit down again. You review your income. You realign your goals. You tweak your spending.

This continuous reset keeps your financial life dynamic, not robotic.

Why This Budgeting Strategy Works in India (Especially Now)

India is rapidly digitising. UPI is everywhere. One tap and your money disappears.

And with social media bombarding you with the next thing to buy, you need more than awareness—you need structure.

Zero-Based Budgeting offers just that.

Especially in 2025, when:

- Inflation continues to eat into middle-class income

- Credit card usage is surging

- Most Indians still don’t have an emergency fund

This strategy gives families the blueprint to thrive, not just survive.

Real-Life Example: Sharma Family, Pune

- Monthly income: ₹85,000

- Goal: Save ₹25,000/month for a house down payment in 3 years

With ZBB:

- ₹10,000 to SIPs

- ₹5,000 to RD

- ₹5,000 to emergency fund

- ₹5,000 to recurring expenses like insurance

Remaining ₹60,000 is carefully allocated to rent, groceries, kids’ education, etc.

No spillovers. No vague “miscellaneous” column.

After 6 months, their savings habits were locked in.

After 12 months, they had ₹3 lakh in liquid investments.

Before ZBB, they struggled to save ₹5,000/month.

Common Mistakes to Avoid

- Not budgeting irregular expenses: Think annual car insurance or Diwali gifts. Break them into monthly chunks.

- Over-optimism: Don’t cut entertainment to ₹0. You’ll snap.

- Skipping tracking: If you don’t monitor, you’ll drift.

Final Thought: Budgeting Strategy or Life Strategy?

Zero-Based Budgeting isn’t just a way to manage your wallet. It’s a mindset.

It trains you to be intentional. To prioritise. To say no without guilt.

And when done right, it’ll do more than fix your finances—it’ll change the way you live.

In a world obsessed with growing income, perhaps the smarter play is managing the income you already have. That’s the promise of this budgeting strategy.

And in 2025, when money leaks from a dozen apps and subscriptions, the only defence you have is clarity. Zero-Based Budgeting offers that clarity. Use it we

know more :- Approaching Zero-Based Budgeting: The Benefits and Challenges You Need to Know

Frequently Asked Questions (FAQs)

1. Is Zero-Based Budgeting only for salaried individuals?

Not at all. Whether you’re a freelancer, small business owner, or homemaker managing a household allowance, Zero-Based Budgeting (ZBB) works across the board. The principle is the same: allocate every rupee with intention, regardless of how your income arrives.

2. Isn’t this too rigid for Indian households with fluctuating expenses?

Actually, ZBB is designed to handle fluctuations. It encourages monthly reassessment, so you adjust your allocations based on real needs. One month you may spend more on health, another month on travel—but you’ll always stay in control.

3. What’s the difference between traditional budgeting and ZBB?

Traditional budgeting starts with expenses and ends with savings (often minimal).

ZBB flips that: you prioritise savings and investments first, and spend what’s left. It’s proactive, not reactive.

4. How do I manage irregular or annual expenses like school fees or festivals?

You break them down. If Diwali shopping costs you ₹12,000 annually, set aside ₹1,000 every month in a separate “Festival Fund.” ZBB ensures you’re never caught off guard.

5. Can I use budgeting apps for ZBB?

Yes, apps like YNAB (You Need A Budget), Walnut, or even Excel/Google Sheets can support a ZBB framework. What matters is the approach, not the tool.

Leave a Reply