The government wants citizens to be financially independent after retirement—and it makes that clear by incentivizing long-term saving. Among all retirement-focused investment options, the National Pension System (NPS) stands out for one key reason: tax benefits. In 2025, this pension scheme continues to attract both salaried employees and self-employed individuals, not just because it ensures retirement security, but because it also offers multiple tax-saving opportunities under the Income Tax Act.

- 1. Tax Benefit Under Section 80CCD(1)

- 2. Additional Deduction Under Section 80CCD(1B)

- 3. Employer’s Contribution – Section 80CCD(2)

- 4. Tax Treatment at Maturity (EEE Status)

- 5. Tier I vs Tier II: Know the Difference

- 6. NPS Compared to Other Tax-Saving Options

- 7. Additional Benefits of the NPS Pension Scheme

- Final Thoughts

- FAQs

- Q1. Can I claim deductions under both Section 80CCD(1) and 80CCD(1B)?

- Q2. Can self-employed individuals claim employer contributions under Section 80CCD(2)?

- Q3. Is the entire NPS corpus tax-free at retirement?

- Q4. What if I exit NPS before the age of 60?

- Q5. Is Tier II NPS account eligible for tax deductions?

- Q6. What is the minimum amount I need to invest in NPS?

- Q7. Can NRIs invest in NPS?

Here’s a detailed look at how you can save taxes using NPS in 2025.

1. Tax Benefit Under Section 80CCD(1)

This section allows individuals to claim deductions on their own contributions to the NPS Tier I account. It falls under the broader umbrella of Section 80C, which caps tax deductions at ₹1.5 lakh.

- Who qualifies? Salaried employees and self-employed individuals

- Deduction limit:

- Salaried individuals – Up to 10% of salary (Basic + DA)

- Self-employed individuals – Up to 20% of gross total income

- Maximum deduction: ₹1.5 lakh (included in Section 80C ceiling)

This provision gives you the same benefit as traditional instruments like ELSS, PPF, and life insurance—but NPS offers more on top of this.

2. Additional Deduction Under Section 80CCD(1B)

This is a special section introduced to promote NPS further. It allows for an additional deduction of ₹50,000 exclusively for contributions made to NPS Tier I.

- Who can claim? Anyone investing in NPS—salaried or self-employed

- Limit: ₹50,000 (over and above the ₹1.5 lakh under Section 80C)

This means the total deduction available through NPS can go up to ₹2 lakh annually, giving it a strong advantage over most other pension schemes.

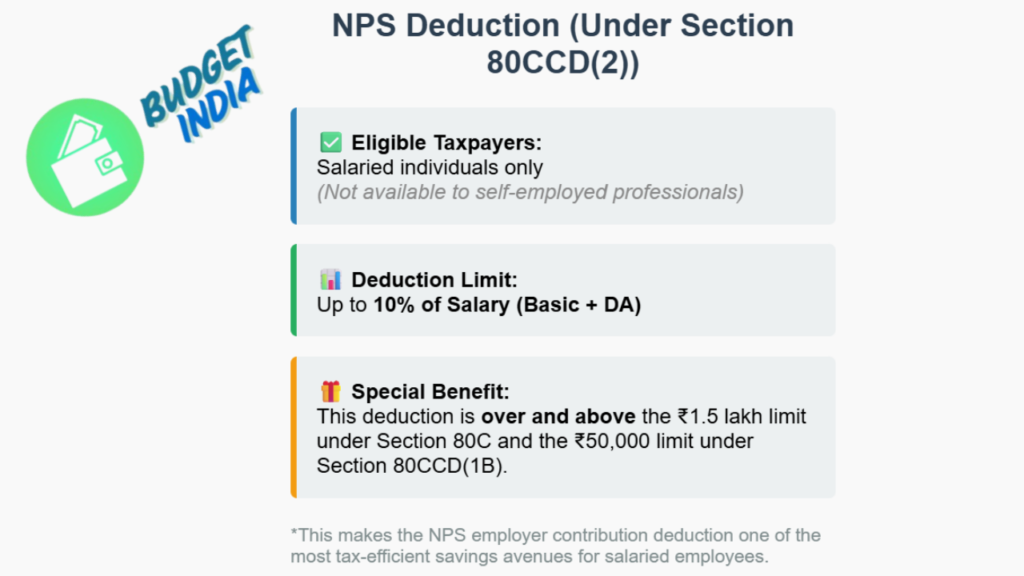

3. Employer’s Contribution – Section 80CCD(2)

If you’re a salaried employee, this section offers an extra layer of tax relief. Contributions made by your employer to your NPS account are fully deductible, up to a defined limit.

- Eligible taxpayers: Salaried individuals (not available to self-employed)

- Deduction limit: Up to 10% of salary (Basic + DA)

- Special benefit: This deduction is not part of the ₹1.5 lakh or ₹2 lakh limit

This employer contribution acts as a tax-free salary component. If your employer offers to contribute to NPS, it’s a win-win for both your retirement and your tax bill.

4. Tax Treatment at Maturity (EEE Status)

The NPS now enjoys what’s known as Exempt-Exempt-Exempt (EEE) status. That means:

- Contributions: Tax deductible

- Returns: Exempt from tax while your funds are growing

- Withdrawal at maturity:

- 60% of the corpus can be withdrawn tax-free at retirement (age 60)

- The remaining 40% must be used to buy an annuity, which is taxable as per your income slab

While the annuity portion is taxable, the bulk of the withdrawal is exempt, making NPS one of the most tax-efficient pension schemes available today.

5. Tier I vs Tier II: Know the Difference

NPS accounts are categorized into two tiers—only one offers tax benefits.

- Tier I Account:

- Meant for retirement savings

- Contributions eligible for tax deductions

- Withdrawal restrictions until age 60

- Tier II Account:

- Works like a savings account

- No tax deductions (except for government employees)

- Funds can be withdrawn anytime

If your goal is tax saving, always choose Tier I.

6. NPS Compared to Other Tax-Saving Options

| Investment Option | Max Deduction | Returns | Tax on Maturity | Lock-in Period |

|---|---|---|---|---|

| NPS | ₹2,00,000 | Market-linked | 60% Tax-Free, 40% Taxable as Annuity | Until age 60 |

| PPF | ₹1,50,000 | Fixed (~7–8%) | Fully Tax-Free | 15 years |

| ELSS | ₹1,50,000 | Market-linked | Taxable after ₹1L (10%) | 3 years |

| EPF | ₹1,50,000 | 8–8.5% | Tax-Free (within limits) | Until retirement/job switch |

| ULIPs | ₹1,50,000 | Market-linked | Depends on policy | 5 years |

Among these, only NPS allows tax saving beyond ₹1.5 lakh, giving it an edge if you’ve already maxed out your 80C limit.

7. Additional Benefits of the NPS Pension Scheme

- Low fees: Fund management costs are among the lowest in the industry (~0.01%)

- Flexibility: Choose between Active (you select asset classes) or Auto (allocation adjusts with age) investment modes

- Equity exposure: Up to 75% allocation allowed in equity under Active Choice

- Account portability: Your NPS account moves with you, even if you change jobs or cities

- Annuity options: Multiple insurers to choose from when buying an annuity post-retirement

These features make NPS a robust pension scheme, not just for tax saving but for overall retirement planning.

Final Thoughts

The National Pension System isn’t just a retirement fund—it’s a smart tax-saving vehicle. With multiple layers of deductions, low cost, and high flexibility, NPS ranks among the top pension schemes in India in 2025.

If you’ve already exhausted your 80C limits or are looking for a retirement plan that doesn’t eat into your current take-home salary, NPS is well worth a serious look. Between tax savings and long-term returns, it offers a balance that few instruments can match.

FAQs

Q1. Can I claim deductions under both Section 80CCD(1) and 80CCD(1B)?

Yes. You can claim up to ₹1.5 lakh under Section 80CCD(1) and an additional ₹50,000 under Section 80CCD(1B), making your total deduction ₹2 lakh.

Q2. Can self-employed individuals claim employer contributions under Section 80CCD(2)?

No. Section 80CCD(2) applies only to salaried individuals receiving employer contributions. Self-employed persons can claim deductions under 80CCD(1) and 80CCD(1B) only.

Q3. Is the entire NPS corpus tax-free at retirement?

Not entirely. 60% of the corpus can be withdrawn tax-free. The remaining 40% must be used to buy an annuity, which is taxed as per your income slab when the annuity is paid.

Q4. What if I exit NPS before the age of 60?

If you exit early:

- Only 20% of the corpus can be withdrawn as a lump sum (tax-free)

- At least 80% must be used to buy an annuity (taxable)

Q5. Is Tier II NPS account eligible for tax deductions?

No, Tier II accounts do not offer tax benefits for most subscribers. Only central government employees may claim deductions under specific conditions.

Q6. What is the minimum amount I need to invest in NPS?

For Tier I accounts:

- Minimum contribution per year: ₹1,000

- Minimum one contribution per year is mandatory to keep the account active

Q7. Can NRIs invest in NPS?

Yes, Non-Resident Indians (NRIs) are eligible to invest in NPS and can claim the same tax benefits, subject to compliance with RBI and FEMA regulations.

Leave a Reply