When it comes to saving taxes in India, most people think of Section 80C investments like PPF, ELSS, or life insurance. But there’s another powerful tool that often goes unnoticed—the National Pension System (NPS). Not only does NPS help you build a retirement corpus, but it also offers significant tax benefits that can reduce your taxable income and save you money.

If you’re looking for a long-term investment option that combines tax savings with retirement planning, NPS is worth considering. In this article, we’ll explore how NPS works, its tax benefits, and how you can use it to save money on income tax. Let’s dive in!

What is NPS?

The National Pension System (NPS) is a government-backed retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It allows you to invest in a mix of equity, corporate bonds, and government securities, offering the potential for higher returns over the long term.

NPS is open to all Indian citizens aged 18-70, including salaried employees, self-employed professionals, and even NRIs. It’s a flexible and low-cost investment option that helps you build a retirement corpus while enjoying tax benefits.

Tax Benefits of NPS

NPS offers triple tax benefits under different sections of the Income Tax Act, making it one of the most tax-efficient investment options in India. Here’s how it works:

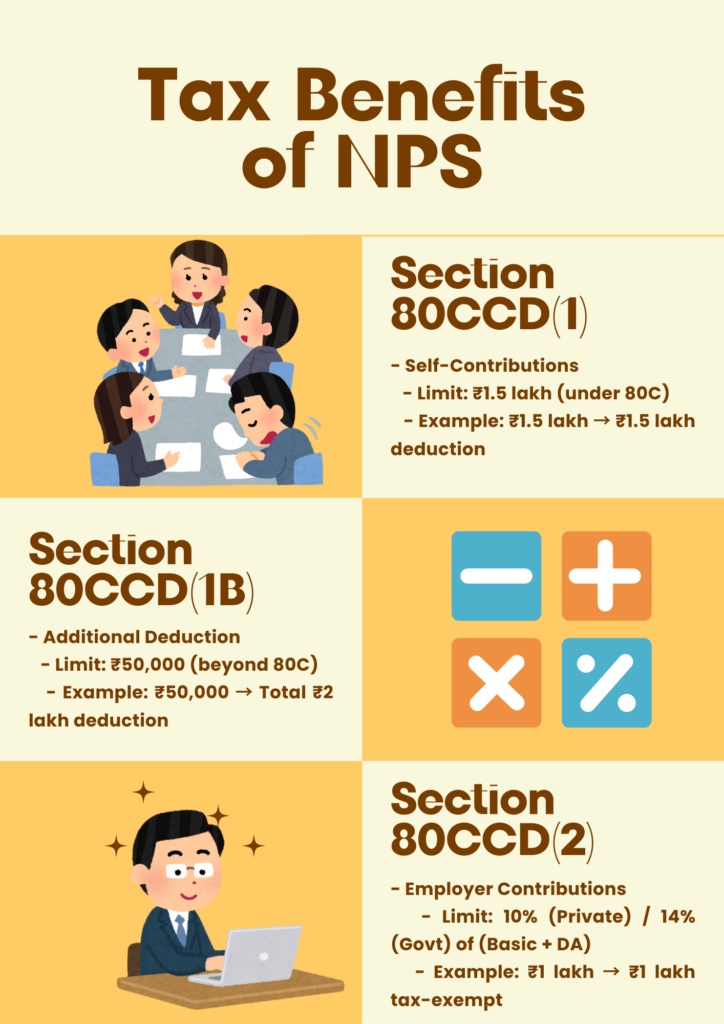

- Section 80CCD(1): Deduction on Self-Contributions

- You can claim a deduction of up to ₹1.5 lakh per financial year for your personal contributions to NPS.

- This deduction falls within the overall Section 80C limit.

- Example: Investing ₹1.5 lakh in NPS allows you to claim a ₹1.5 lakh deduction under Section 80CCD(1).

2. Section 80CCD(1B): Additional Deduction

- An additional deduction of ₹50,000 per financial year is available under Section 80CCD(1B) for NPS contributions.

- This is separate from and beyond the ₹1.5 lakh limit under Section 80C.

- Example: If you invest an additional ₹50,000 in NPS, you can claim a total deduction of ₹2 lakh (₹1.5 lakh under 80CCD(1) + ₹50,000 under 80CCD(1B)).

3. Section 80CCD(2): Employer Contributions

- For salaried employees, employer contributions to NPS (up to 10% of basic salary + DA for private employees, and 14% for central government employees) are tax-free.

- This is in addition to the Section 80C limit.

- Example: If an employer contributes ₹1 lakh (within the applicable percentage), this amount is tax-exempt.

How NPS Helps You Save Tax

Let’s understand the tax-saving potential of NPS with an example:

- Annual Income: ₹12 lakh

- NPS Contribution (Self): ₹50,000

- NPS Contribution (Employer): ₹1 lakh

| Section | Deduction Amount (₹) |

|---|---|

| Section 80CCD(1) | 50,000 |

| Section 80CCD(1B) | 50,000 |

| Section 80CCD(2) | 1,00,000 |

| Total Deduction | 2,00,000 |

By investing in NPS, you can reduce your taxable income by ₹2 lakh, saving up to ₹62,400 in taxes (assuming a 30% tax rate).

Other Benefits of NPS

- Flexibility: You can choose your asset allocation (equity, corporate bonds, or government securities) based on your risk appetite.

- Low Cost: NPS has one of the lowest fund management charges (0.01% per annum).

- Portability: You can continue your NPS account even if you change jobs or locations.

- Retirement Corpus: At retirement, you can withdraw 60% of the corpus tax-free and use the remaining 40% to buy an annuity for a regular pension.

How to Open an NPS Account

Opening an NPS account is simple and can be done online or offline. Here’s how:

Online Process

- Visit the official NPS website (enps.nsdl.com).

- Register using your PAN and Aadhaar.

- Choose your Pension Fund Manager (PFM) and asset allocation.

- Make the initial contribution (minimum ₹500).

Offline Process

- Visit a Point of Presence (PoP) like a bank or post office.

- Fill out the NPS application form.

- Submit KYC documents (PAN, Aadhaar, and address proof).

- Make the initial contribution.

Tips to Maximize NPS Benefits

- Start Early: The earlier you start, the more time your investments have to grow.

- Increase Contributions Gradually: As your income grows, increase your NPS contributions to maximize tax benefits.

- Choose the Right Asset Allocation: If you’re young, consider a higher equity allocation for better returns.

- Track Your Investments: Regularly review your NPS account and make adjustments as needed.

Common Myths About NPS

- Myth: NPS is only for government employees.

Fact: NPS is open to all Indian citizens, including private sector employees and self-employed professionals. - Myth: NPS returns are not guaranteed.

Fact: While NPS returns are market-linked, the long-term performance has been competitive. - Myth: You can’t withdraw money before retirement.

Fact: Partial withdrawals are allowed for specific purposes like education, marriage, or medical emergencies.

FAQs About NPS

1. Is NPS better than PPF?

NPS offers higher potential returns and additional tax benefits, but PPF is safer and offers guaranteed returns. Choose based on your risk appetite and financial goals.

2. Can I withdraw my NPS corpus before retirement?

Yes, but only up to 25% of your contributions for specific purposes after 3 years.

3. What happens to my NPS account if I change jobs?

Your NPS account remains active, and you can continue contributing to it.

4. Is NPS taxable at withdrawal?

60% of the corpus is tax-free at withdrawal, while the remaining 40% must be used to buy an annuity (pension).

Final Thoughts

The National Pension System (NPS) is a powerful tool for both retirement planning and tax savings. With its triple tax benefits, low costs, and flexibility, it’s an excellent option for anyone looking to build a secure financial future while reducing their tax liability.

Whether you’re a salaried employee or self-employed, consider including NPS in your financial portfolio. Start early, contribute regularly, and watch your retirement corpus grow while saving money on taxes. After all, a secure retirement is the best gift you can give yourself!

Leave a Reply