In the current evolving economic landscape, a savings accounts is no longer just a safe haven for excess cash—it has become a strategic avenue for generating passive earnings. With inflation trending upward and traditional fixed deposits offering moderate returns, numerous Indian financial institutions are now presenting high-interest savings options that rival short-term investments.

For individuals prioritizing liquidity, capital safety, and attractive interest earnings, choosing a high-yield savings account in 2025 is a calculated decision. This detailed guide outlines a handpicked list of the 14 most rewarding savings accounts in India, offering comprehensive evaluations of their interest rates, account characteristics, minimum deposit conditions, and online banking capabilities.

- Top 14 High-Yield Savings Accounts Options in India (2025)

- 1. AU Small Finance Bank

- 2. IDFC FIRST Bank

- 3. Equitas Small Finance Bank

- 4. Ujjivan Small Finance Bank

- 5. Jana Small Finance Bank

- 6. ESAF Small Finance Bank

- 7. Fincare Small Finance Bank

- 8. Suryoday Small Finance Bank

- 9. North East Small Finance Bank

- 10. RBL Bank

- 11. Yes Bank

- 12. IndusInd Bank

- 13. Kotak Mahindra Bank (811 Edge)

- 14. State Bank of India – Savings Plus Account

- 📈 Comparative Snapshot of Interest Rates – 2025

- Tax Considerations on Savings Account Interest

- Guidelines to Choose the Best High-Yield Savings Account

- ✅ Final Thoughts: Where to Park Your Savings in 2025?

- Frequently Asked Questions (FAQs)

- 1. Are high-interest savings accounts safe in India?

- 2. How frequently is interest credited in savings accounts?

- 3. Do high-interest rates come with hidden charges or conditions?

- 4. Which is better: savings accounts with high interest or fixed deposits?

- 5. Can NRIs open high-interest savings accounts in India?

Top 14 High-Yield Savings Accounts Options in India (2025)

1. AU Small Finance Bank

- Peak Interest Rate: Up to 7.25% per annum

- Average Monthly Balance Requirement: ₹5,000

- Major Benefits:

- Among the best interest rates nationwide

- Seamless digital banking tools

- Quarterly interest credit

- Best For: Digitally inclined savers aiming for optimal returns without losing flexibility.

2. IDFC FIRST Bank

- Interest Band: Up to 7.00% p.a.

- Minimum Balance Obligation: ₹10,000

- Key Differentiators:

- Daily interest accrual—rare in Indian banking

- Unlimited free ATM usage

- Feature-rich mobile platform

- Ideal For: Those who value daily compounding and frictionless banking.

3. Equitas Small Finance Bank

- Highest Interest Rate: Up to 7.00% per annum

- Minimum Balance Need: ₹5,000

- Core Advantages:

- Cashback incentives on debit card transactions

- Monthly interest payouts

- Digital zero-balance accounts

- Best Choice For: Users preferring monthly credits and a digital-centric banking style.

4. Ujjivan Small Finance Bank

- Top Interest Offered: 7.00% p.a.

- Required Balance Range: ₹1,000 to ₹5,000

- Distinct Offerings:

- Affordable entry for rural/underbanked regions

- Easy-to-use mobile interface

- Reliable branch and customer support

- Preferred By: New savers and those in non-metro areas seeking value.

5. Jana Small Finance Bank

- Max Rate Provided: Up to 7.00% annually

- Monthly Balance Requirement: ₹2,000–₹10,000 (account dependent)

- Highlights:

- Free NEFT/RTGS/IMPS transfers

- Video KYC-enabled account setup

- Variety of account types for singles and joint holders

- Perfect For: Customers wanting versatile account choices and digital-physical flexibility.

6. ESAF Small Finance Bank

- Top Yield Rate: Up to 7.00% per annum

- Minimum Required Deposit: ₹1,000

- Unique Pros:

- Auto-sweep functionality linked to FDs

- Secure mobile access and instant alerts

- Focused support for underserved communities

- Great Option For: Tier 2/3 city investors emphasizing inclusive banking.

7. Fincare Small Finance Bank

- Max Interest Yield: Up to 7.00% p.a.

- Balance Prerequisite: ₹2,000–₹5,000

- Account Merits:

- Automatic FD sweep functionality

- Intuitive and responsive app interface

- Simplified onboarding for diverse geographies

- Recommended For: High-interest seekers who appreciate linked FD benefits.

8. Suryoday Small Finance Bank

- Highest Interest Available: 6.75% annually

- Required Minimum Balance: ₹1,000

- Key Utilities:

- Interest credited every month

- 24/7 access via a dedicated app

- Zero-balance accounts for salaried users

- Best Fit For: Those who value frequent interest payouts.

9. North East Small Finance Bank

- Top Rate Offered: 6.75% per annum

- Balance Requirement: ₹2,500

- Key Traits:

- Serves far-flung and semi-urban populations

- Hassle-free account initiation

- Regional focus with a community-first ethos

- Suited For: Residents of northeastern India seeking reliable local banking.

10. RBL Bank

- Max Interest Rate: 6.50% p.a.

- Required Monthly Balance: ₹5,000–₹10,000

- Top Attributes:

- Monthly payout of interest

- Debit card rewards and insurance coverage

- Streamlined digital interface

- Who Should Opt: Lifestyle-oriented customers who want both perks and profits.

11. Yes Bank

- Interest Cap: 6.25% p.a.

- Minimum Balance Mandate: ₹10,000

- Core Benefits:

- Complimentary digital fund transfers

- Included accident insurance

- Instant digital account setup

- Suitable For: Users seeking secure returns with tech-enabled banking.

12. IndusInd Bank

- Best Offered Rate: Up to 6.00% per annum

- Minimum Balance Guideline: ₹10,000

- Highlights:

- Personalized account number option

- Automatic FD conversion for surplus funds

- Smooth mobile and web access

- Go For It If: You prioritize personalization and modern features.

13. Kotak Mahindra Bank (811 Edge)

- Interest Rate Ceiling: Up to 4.00% p.a.

- Minimum Balance Level: ₹10,000 (Edge account)

- Main Advantages:

- Fully online account activation

- Expense tracking via mobile app

- Exclusive e-commerce benefits

- Best For: Tech-savvy users wanting ease and security.

14. State Bank of India – Savings Plus Account

- Base Interest Rate: 2.70% p.a.

- With Sweep FD: Up to 6.50% p.a.

- Minimum Balance Standard: ₹3,000 (urban), ₹2,000 (semi-urban)

- Advantages:

- Sweep facility enhances interest on idle money

- Extensive ATM and branch reach

- Trustworthiness of a leading public sector bank

- Recommended For: Risk-averse savers emphasizing safety and reach.

📈 Comparative Snapshot of Interest Rates – 2025

| Bank | Highest Interest Rate | Minimum Balance Requirement |

|---|---|---|

| AU Small Finance Bank | 7.25% p.a. | ₹5,000 |

| IDFC FIRST Bank | 7.00% p.a. | ₹10,000 |

| Equitas Small Finance Bank | 7.00% p.a. | ₹5,000 |

| Ujjivan Small Finance Bank | 7.00% p.a. | ₹1,000 |

| Jana Small Finance Bank | 7.00% p.a. | ₹2,000 |

| ESAF Small Finance Bank | 7.00% p.a. | ₹1,000 |

| Fincare Small Finance Bank | 7.00% p.a. | ₹2,000 |

| Suryoday Small Finance Bank | 6.75% p.a. | ₹1,000 |

| North East Small Finance Bank | 6.75% p.a. | ₹2,500 |

| RBL Bank | 6.50% p.a. | ₹5,000 |

| Yes Bank | 6.25% p.a. | ₹10,000 |

| IndusInd Bank | 6.00% p.a. | ₹10,000 |

| Kotak Mahindra Bank | 4.00% p.a. | ₹10,000 |

| SBI Savings Plus (Auto FD) | Up to 6.50% p.a. | ₹3,000 |

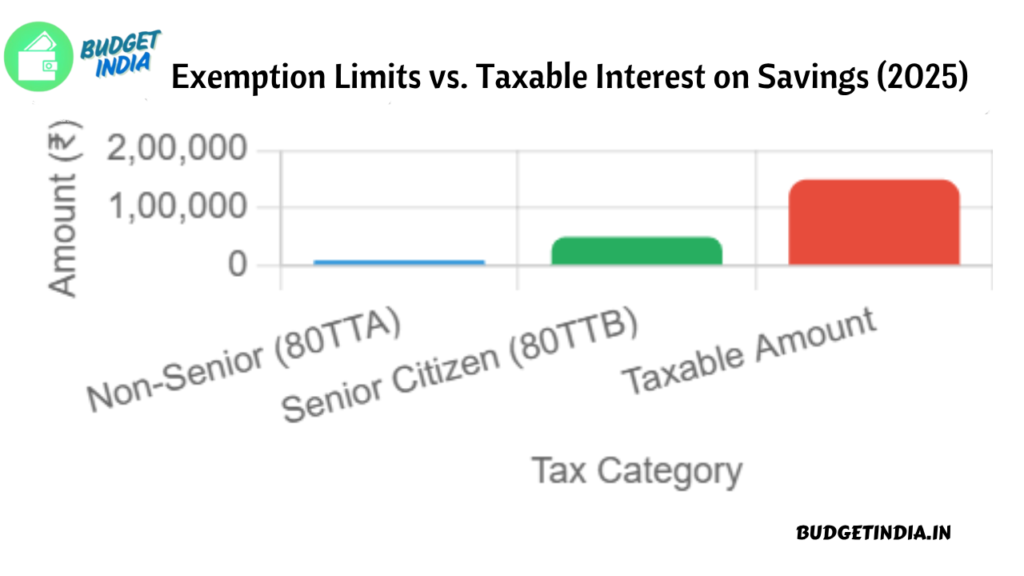

Tax Considerations on Savings Account Interest

- Earnings up to ₹10,000 yearly are exempt under Section 80TTA (for non-seniors).

- Seniors are eligible for an exemption of up to ₹50,000 under Section 80TTB.

- Interest exceeding these caps is taxed according to your income tax bracket.

Guidelines to Choose the Best High-Yield Savings Account

- Compare frequency of interest credit (daily, monthly, quarterly)

- Choose accounts with sweep-in options to FDs

- Assess app ratings and online service quality

- Confirm RBI license and DICGC insurance (₹5 lakh protection)

- Watch for hidden charges, ATM fees, and maintenance costs

✅ Final Thoughts: Where to Park Your Savings in 2025?

Selecting the right savings account involves more than just interest rate comparisons. Factors like digital experience, service quality, and fund safety are equally critical. For those focused solely on interest, AU Small Finance Bank and IDFC FIRST Bank stand out. Meanwhile, if you’re seeking a secure and well-rounded option, banks like IndusInd Bank and SBI’s Savings Plus merit consideration.

Assess your priorities, compare comprehensively, and opt for the account that resonates with your financial goals.

Frequently Asked Questions (FAQs)

1. Are high-interest savings accounts safe in India?

Yes, high-interest savings accounts offered by RBI-licensed banks, including small finance banks, are generally safe. Deposits up to ₹5 lakh per individual per bank are insured under the Deposit Insurance and Credit Guarantee Corporation (DICGC) scheme.

2. How frequently is interest credited in savings accounts?

The interest is usually credited quarterly or monthly, depending on the bank’s policy. Some modern banks, like IDFC FIRST Bank or Equitas, offer monthly or even daily interest accrual for faster compounding benefits.

3. Do high-interest rates come with hidden charges or conditions?

Often, yes. High-interest accounts may require a higher minimum balance or restrict benefits below certain thresholds. It’s essential to read the fine print, especially around balance slabs, maintenance fees, and transaction limits.

4. Which is better: savings accounts with high interest or fixed deposits?

Savings accounts offer higher liquidity and ease of withdrawal, while fixed deposits may offer slightly higher returns but with lock-in periods. A hybrid option, like an auto-sweep account (e.g., SBI Savings Plus), combines both benefits.

5. Can NRIs open high-interest savings accounts in India?

Yes, NRIs can open NRE or NRO savings accounts in select banks offering competitive interest rates. However, interest earned on NRO accounts is taxable in India, whereas NRE account interest is tax-free

Leave a Reply