Uncertainty is a part of life. Unexpected medical issues, layoffs, or urgent home repairs can place a heavy burden on your finances. In 2025, with rising inflation and job insecurity, creating emergency savings in India has become a core part of responsible financial planning. It provides a protective layer against economic shocks.

This guide offers a step-by-step plan to help you establish your emergency savings, answers a key question—“How much money should I keep in my emergency fund in India?”—and outlines the best practices to follow in 2025.

Why Emergency Savings Are Vital in Financial Planning

A contingency fund works as a buffer against unforeseen monetary setbacks. Without one, you may have to resort to borrowing at high interest rates or prematurely cashing out long-term investments. By having emergency savings in place, you maintain control over your finances without derailing your broader financial goals.

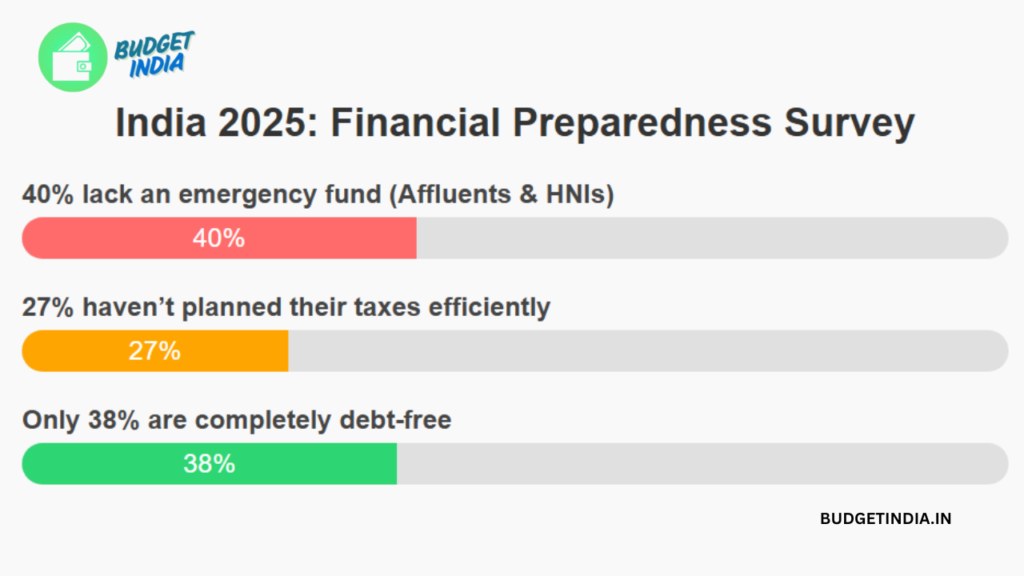

Fact: According to Finnovate, a financial fitness platform, a recent survey reveals critical gaps in financial preparedness—about 40% of affluent and HNI Indians lack a proper emergency fund, 27% have not planned taxes efficiently, and only 38% are completely debt-free.

How Much Money Should You Keep in Your Emergency Savings in India?

This question tops the list for individuals planning finances in India 2025.

General Recommendation:

Most financial advisors suggest maintaining between 3 to 6 months of essential household expenses.

Tailored Suggestions:

- Salaried professionals with stable employment: Save 3–6 months of basic expenses

- Single-earner or dependent families: Keep aside 6–12 months

- Freelancers or business owners with inconsistent income: Target 9–12 months of living costs

For example, if your essential monthly outgo is ₹40,000:

- Minimum backup: ₹1.2 lakhs (3 months)

- Balanced reserve: ₹2.4 lakhs (6 months)

- High-security buffer: ₹4.8 lakhs (12 months)

Make adjustments based on your career stability, health conditions, dependents, and financial obligations.

Step-by-Step Approach to Build Emergency Savings

1. Calculate Monthly Necessities

List non-negotiable expenses—rent, groceries, premiums, children’s school fees, EMIs, and transport. Skip leisure-related spending.

2. Set a Savings Target

Multiply your monthly essentials by the number of months you intend to cover. Six months is a commonly suggested target for most earners.

3. Start Small and Be Consistent

Even saving ₹2,000–₹5,000 monthly makes a big difference over time. Consistency matters more than the starting amount.

4. Choose the Right Parking Options

Your emergency fund must be:

- Safe

- Easy to access

- Separate from regular-use accounts

Recommended options in India 2025:

- High-yield savings accounts (e.g., AU Small Finance Bank, Ujjivan SFB)

- Flexible fixed deposits with premature withdrawal allowed

- Liquid mutual funds (low-risk and easy redemption)

- Recurring deposits for disciplined contributions

5. Automate the Contribution

Enable an automatic debit from your primary account to your emergency savings. Treat it like a utility bill.

6. Use Only in Real Emergencies

Restrict access to critical scenarios—such as hospitalization, temporary job loss, or major repairs. You can even name the account “For Emergency Only” to discourage casual withdrawals.

7. Monitor and Refill as Needed

Review the fund every 6 to 12 months. If you withdraw any amount, prioritize refilling it at the earliest.

Where Not to Park Your Emergency Savings

Avoid locking your emergency corpus in:

- Stock market or equity mutual funds – exposed to volatility

- Long-term fixed deposits with penalties on early exit

- Physical gold or property – difficult to liquidate quickly

Benefits of Emergency Savings in Financial Planning

- Shields long-term investment strategies from disruption

- Reduces reliance on costly credit or loans

- Lowers anxiety during tough financial phases

- Helps make better decisions without panic

Conclusion

As we move through 2025, financial planning in India demands resilience. Emergency savings are the first step toward financial independence and security. By saving gradually and using the right tools, you can safeguard yourself and your loved ones against unexpected hardships.

Act now—because financial preparedness today means peace of mind tomorrow.

FAQS:

1. How much should I save in my emergency fund?

It’s recommended to save at least three to six months’ worth of essential living expenses. If you’re a freelancer, business owner, or have irregular income, aim for 9–12 months’ worth of expenses.

2. Where should I keep my emergency fund?

Your emergency fund should be kept in a safe, easily accessible, and liquid instrument. Consider high-interest savings accounts, liquid mutual funds, or flexible fixed deposits that allow premature withdrawals without penalties.

3. Can I use my emergency fund for non-emergency situations?

No, your emergency fund should only be used for true emergencies, such as health crises, job loss, or urgent repairs. Avoid using it for vacations, gadget purchases, or other discretionary expenses.

4. How do I build my emergency fund if I have limited income?

Start small, even ₹1,000 or ₹2,000 per month. As your financial situation improves, gradually increase the amount. Automating your savings can also make it easier to stick to your goal.

5. Should I adjust my emergency fund amount based on my job stability?

Yes, if you have an unstable job or are self-employed, consider saving a higher amount (9–12 months of expenses) for additional security.

6. What is the best way to grow my emergency fund?

Look for high-yield savings accounts or liquid mutual funds for slightly higher returns with minimal risk. Remember, the priority is liquidity and safety, not high returns.

Leave a Reply