Section 80C of the Indian Income Tax Act is a widely used legal tool that enables taxpayers to curtail their taxable income by making specific investments or incurring qualified expenditures. This section offers tax saving deductions of up to ₹1.5 lakh per annum, providing individuals and Hindu Undivided Families (HUFs) the opportunity to systematically manage their tax liabilities while promoting long-term financial planning. By leveraging Section 80C, taxpayers can not only reduce their income tax burden but also build a disciplined approach toward wealth creation and tax saving investments.

- Overview of Section 80C

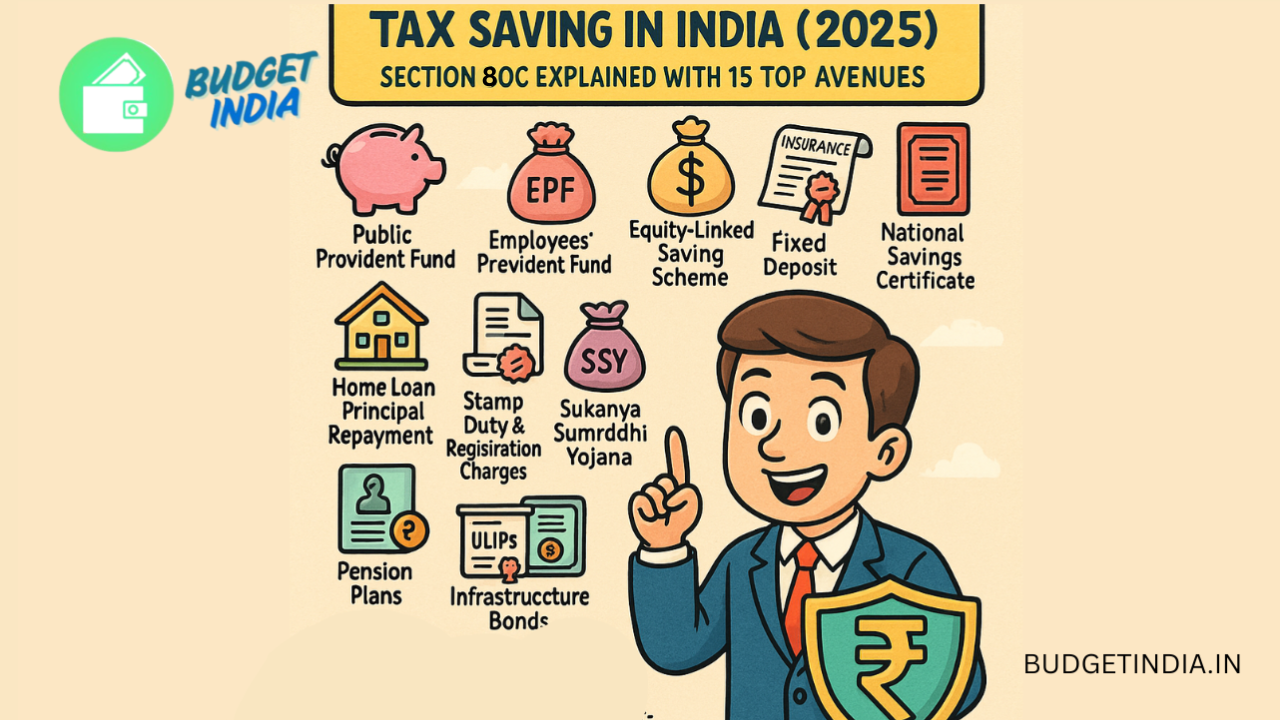

- Top 15 Tax Saving Methods Under Section 80C for FY 2025

- 1. Public Provident Fund (PPF)

- 2. Employees' Provident Fund (EPF)

- 3. Equity-Linked Saving Scheme (ELSS)

- 4. Life Insurance Premiums

- 5. National Savings Certificate (NSC)

- 6. Tax Saving Fixed Deposits (FDs)

- 7. Sukanya Samriddhi Yojana (SSY)

- 8. Senior Citizens Savings Scheme (SCSS)

- 9. Home Loan Principal Repayment

- 10. Stamp Duty & Registration Charges

- 11. Children’s Education Fees

- 12. Unit Linked Insurance Plans (ULIPs)

- 13. Pension Plans from Life Insurers

- 14. Infrastructure Bonds (If Notified)

- 15. Government-Notified Bonds (e.g., NABARD/REC)

- Pro Tips to Maximize Your Tax Saving Under Section 80C

- Final Thoughts

- Frequently Asked Questions (FAQs)

Overview of Section 80C

Section 80C grants income deductions from your gross total earnings, allowing you to lower your tax burden when you opt for the older tax structure. It is not applicable under the new income tax regime introduced in 2020.

- Maximum Deduction Permissible: ₹1,50,000 annually

- Eligible Taxpayers: Individuals and HUFs

- Applicable Framework: Only under the traditional tax system

Top 15 Tax Saving Methods Under Section 80C for FY 2025

1. Public Provident Fund (PPF)

A government-supported, long-duration investment scheme that offers fixed returns, tax exemptions, and safety.

- Minimum yearly deposit: ₹500

- Lock-in tenure: 15 years (extendable by 5-year intervals)

- Interest rate: Government-revised quarterly (currently around 7.1%)

Benefits:

- Full tax immunity: Principal, interest, and maturity are all tax-exempt (EEE status)

- Ideal for low-risk investors focused on retirement or wealth accumulation

- Sovereign guarantee ensures capital security

2. Employees’ Provident Fund (EPF)

A compulsory savings mechanism for salaried employees, where a portion of the salary is deposited each month.

- Employee contributes 12% of basic salary; matched by employer

- Interest rates declared annually by EPFO

Benefits:

- Builds a retirement corpus

- Interest and maturity amount are tax-free up to certain limits

- Contribution by employee is deductible under 80C

3. Equity-Linked Saving Scheme (ELSS)

Mutual funds primarily investing in equity with a 3-year mandatory holding period, offering tax deductions and market-linked returns.

- Shortest lock-in among 80C options (3 years)

- Flexible SIP and lump-sum investment options

Benefits:

- High return potential through equity exposure

- Suitable for growth-focused investors

- Helps build wealth while saving tax

4. Life Insurance Premiums

Premiums paid toward insurance policies qualify for deductions when the policy is in your name, your spouse’s, or your children’s.

- Deduction only if premium is less than 10% of the sum assured

- Applicable to term, endowment, and ULIP policies

Benefits:

- Provides financial security for loved ones

- Combines protection and tax efficiency

- Ensures long-term savings with life cover

5. National Savings Certificate (NSC)

A fixed-income saving instrument available at post offices with guaranteed returns and government backing.

- Maturity: 5 years

- Interest is taxable but reinvested (also deductible under 80C)

Benefits:

- Safe and stable returns

- Ideal for conservative investors

- Easy to purchase and manage

6. Tax Saving Fixed Deposits (FDs)

Time deposits offered by banks that have a five-year lock-in and offer predetermined returns.

- Fixed interest rate

- Interest is taxable, but the principal is deductible under 80C

Benefits:

- Simple and secure investment

- Predictable earnings

- Suitable for non-risk-taking investors

7. Sukanya Samriddhi Yojana (SSY)

A girl child welfare saving scheme offering attractive returns and tax relief.

- For girl children below 10 years

- Maturity upon reaching 21 years of age

- High interest (above 8%, reviewed quarterly)

Benefits:

- Promotes financial readiness for girl’s education or marriage

- Exempt-exempt-exempt (EEE) status

- Encourages long-term disciplined saving

8. Senior Citizens Savings Scheme (SCSS)

Tailored for individuals aged 60 and above, this scheme provides quarterly interest payouts and capital safety.

- Tenure: 5 years (extendable by 3 years)

- Max investment: ₹30 lakh (subject to prevailing limits)

Benefits:

- Consistent income post-retirement

- Backed by the government

- Higher interest than most bank FDs

9. Home Loan Principal Repayment

The portion of EMI paid toward the principal on a home loan is deductible under 80C.

- Only principal amount qualifies

- Property must not be sold within 5 years to retain benefit

Benefits:

- Encourages home ownership

- Reduces taxable income

- Complements Section 24(b) which offers deduction on interest

10. Stamp Duty & Registration Charges

Expenses related to property registration can also be claimed under 80C.

- One-time benefit in the year the payment is made

- Applicable only on residential properties

Benefits:

- Eases the financial burden of property acquisition

- Often overlooked but substantial in tax saving

11. Children’s Education Fees

Tuition fees for up to two children enrolled in full-time education are tax-deductible.

- Only tuition (not donations, transportation, or other charges) is eligible

- Institution must be situated in India

Benefits:

- Directly reduces costs of formal education

- Useful for salaried individuals and professionals with families

12. Unit Linked Insurance Plans (ULIPs)

A hybrid product that combines insurance coverage with market-linked investments.

- Minimum lock-in of 5 years

- Flexible fund options (equity, debt, or balanced)

Benefits:

- Dual benefit: wealth generation and life insurance

- Returns are market-driven

- Suitable for long-term financial planning

13. Pension Plans from Life Insurers

Retirement-oriented insurance products where premiums are eligible for tax relief under 80C and sometimes 80CCC.

- Payout begins upon retirement or maturity

- Corpus can be converted to annuity

Benefits:

- Builds a retirement fund

- Encourages early and regular retirement planning

- Peace of mind in old age

14. Infrastructure Bonds (If Notified)

Long-term bonds issued by public sector undertakings may be notified as eligible for 80C deductions.

- Notified occasionally by the government

- Lock-in typically ranges from 5 to 10 years

Benefits:

- Contribute to national infrastructure development

- Secure and reliable with moderate returns

15. Government-Notified Bonds (e.g., NABARD/REC)

Bonds from approved government agencies can sometimes be included under 80C deductions.

- Available only when explicitly listed under 80C provisions

- Typically carry a fixed interest

Benefits:

- Secure investments backed by public institutions

- Low-risk with stable yield

- Diversifies tax-saving portfolio

Pro Tips to Maximize Your Tax Saving Under Section 80C

- Begin early in the year to spread investments efficiently

- Diversify your portfolio across risk levels (e.g., ELSS + PPF + Insurance)

- Avoid over-investing in a single instrument

- Match investments to your life goals like education, retirement, or home ownership

- Review annually to optimize returns and benefits

Final Thoughts

Utilizing Section 80C efficiently is a smart strategy for reducing your tax liability while investing for your future. Whether your focus is on building a retirement corpus, funding your child’s education, or securing your family’s future, there are multiple reliable and rewarding options to choose from. Strategic planning, diversification, and timely investments can help you take full advantage of the deductions offered under Section 80C in 2025.

Frequently Asked Questions (FAQs)

Q1. Can I use Section 80C under the new tax regime?

No, 80C deductions are only valid if you select the older tax system.

Q2. What’s the highest amount I can deduct under 80C?

Up to ₹1.5 lakh in one financial year.

Q3. Are ELSS returns taxable?

Returns up to ₹1 lakh annually are tax-free; above that, 10% LTCG tax applies.

Q4. Can I claim 80C for more than two children’s tuition fees?

No, the law permits deduction only for up to two children.

Q5. What happens if I invest less than ₹1.5 lakh?

You’ll only receive a deduction for the actual amount you’ve invested.

Leave a Reply