You don’t have to look far to understand why your Credit score matters. It’s the first thing a bank looks at before lending you money. Whether you’re applying for a home loan, car loan, or a credit card with decent benefits, your creditworthiness is defined by this three-digit number. And in a world driven by EMIs and digital lending, a low score doesn’t just hurt—it closes doors.

Now here’s the thing. Improving your CIBIL score isn’t rocket science, but it’s also not something that changes overnight. It requires precision, planning, and a dash of discipline. That said, if you’re looking to boost your score quickly—say, in a matter of weeks or a couple of months—this guide lays out exactly how to go about it.

Let’s get into it.

- What is a CIBIL Score and Why Does It Matter?

- 🔍 Step-by-Step Guide to Improve Your CIBIL Score Quickly in 2025

- 1. Check Your CIBIL Report for Errors – And Fix Them

- 2. Pay Off Outstanding Dues—Especially Credit Cards

- 3. Reduce Your Credit Utilisation Ratio

- 4. Never Miss EMI Payments—Even by a Day

- 5. Avoid Applying for Multiple Loans or Cards in a Short Time

- 6. Diversify Your Credit Mix

- 7. Become an Authorised User on a Good Account

- 8. Consider a Secured Credit Card

- How Long Will It Take to See Results?

- Final Thoughts: Credit Score is a Long Game—but Starts with a Fast Move

- FAQs

What is a CIBIL Score and Why Does It Matter?

Your CIBIL score is a three-digit summary of your credit history, ranging from 300 to 900. The closer you are to 900, the more financially trustworthy you appear. A score above 750 is generally considered excellent.

But here’s what most people miss—your score doesn’t just determine whether you get a loan; it also decides how much interest you pay. A better score equals better terms. Lower EMIs. Faster approvals.

In 2025, as NBFCs and fintech players dominate the lending space, creditworthiness is currency.

Want to know more about it visit : Explained: What is a CIBIL score? Why is it important? – Hindustan Times

🔍 Step-by-Step Guide to Improve Your CIBIL Score Quickly in 2025

1. Check Your CIBIL Report for Errors – And Fix Them

You can’t fix what you don’t know.

Start by downloading your CIBIL report (you get one free report per year). Look for any of the following:

- Incorrect outstanding amounts

- Duplicate loan entries

- Closed accounts shown as active

- Delayed payment records you don’t recognise

If you spot any mistakes, raise a dispute immediately with CIBIL or through your lender. Rectifying these errors alone can give your score a quick 20–30 point bump.

Pro tip: Follow up rigorously. Corrections usually take 15 to 30 days.

2. Pay Off Outstanding Dues—Especially Credit Cards

Credit card debt is poison for your credit score. The longer the dues stay unpaid, the harder your score drops. If you’re carrying any balance, make it a priority to clear at least the minimum due immediately, then work toward full repayment.

Why it works: Payment history contributes nearly 35% to your CIBIL score.

Even one late payment can cost you dearly.

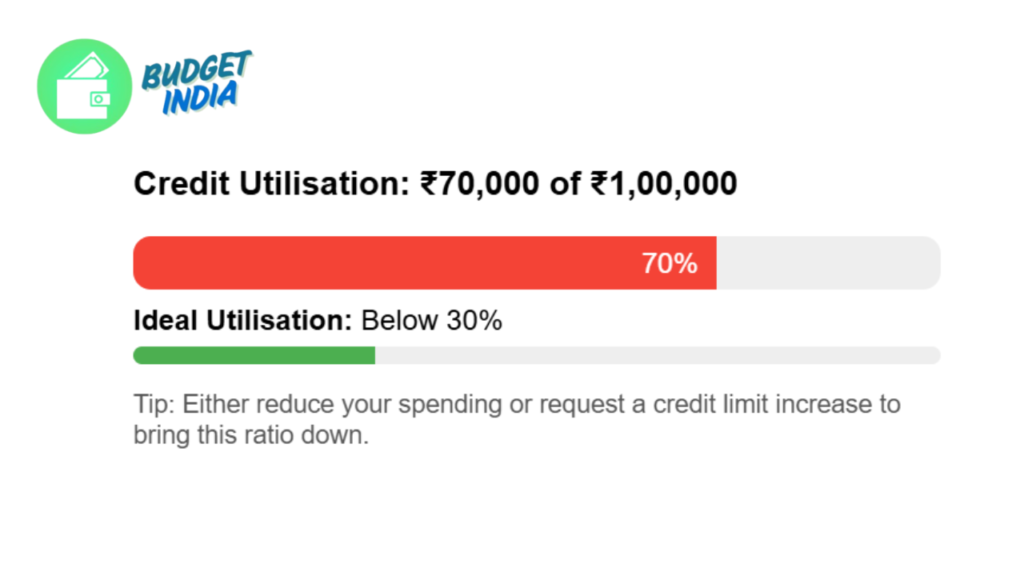

3. Reduce Your Credit Utilisation Ratio

Let’s say you have a credit card limit of ₹1,00,000. If you’re using ₹70,000 every month, you’re at 70% utilisation—and that’s too high.

Try to keep this ratio under 30%. Either reduce your spending or increase your credit limit. Most banks are open to limit hikes if you’ve had a clean repayment track.

Quick fix: Ask for a temporary credit limit enhancement. You don’t even need to use it—just having a higher limit lowers your ratio.

4. Never Miss EMI Payments—Even by a Day

Missing an EMI by even 1 day? That’s enough to get flagged. And once your name goes into the “DPD” (Days Past Due) category, it stays on your report for years.

Set up auto-debit mandates for all loan EMIs and credit card bills. Let your bank do the remembering.

5. Avoid Applying for Multiple Loans or Cards in a Short Time

Every time you apply for a loan, lenders pull a “hard enquiry” on your credit report. Too many of these make you look credit-hungry—and that’s a red flag.

In 2025, with instant loan apps flooding the market, it’s tempting to try your luck everywhere. Don’t. Space out applications and only apply when you’re reasonably sure of approval.

6. Diversify Your Credit Mix

Having just one type of credit (say, only credit cards or only personal loans) doesn’t give lenders a full picture. Try to build a healthy credit portfolio that includes:

- A credit card

- A personal loan

- A secured loan (home loan, gold loan, etc.)

Even taking a small consumer durable loan and repaying it on time helps establish a pattern of trust.

7. Become an Authorised User on a Good Account

If a family member or spouse has an excellent credit history, ask them to add you as an authorised user on their credit card. Their good payment history can rub off on you.

But be careful—this works both ways. If they default, you take a hit too.

8. Consider a Secured Credit Card

If your score is really low (<600), start fresh with a secured credit card backed by a fixed deposit. Use it diligently, pay your bills in full, and within 6 months, you’ll see improvement.

Bonus: These cards are available from SBI, Axis, ICICI and other major banks without any income proof requirement.

How Long Will It Take to See Results?

Improving your CIBIL score isn’t a one-day affair, but you can start seeing changes in 30–60 days if:

- You clear dues immediately

- Dispute and fix errors quickly

- Avoid new hard enquiries

Substantial improvement (say from 600 to 750+) typically takes 6–12 months, but the early gains are the easiest and fastest to achieve.

Final Thoughts: Credit Score is a Long Game—but Starts with a Fast Move

A lot of people make the mistake of ignoring their credit score until they need a loan. But by then, it’s usually too late to make a meaningful change. The real hack? Start fixing it before you need it.

Just like Amazon uses Prime to lock in customer loyalty, banks use CIBIL to decide who gets access to affordable credit. If you can show them that you’re trustworthy—even if it means fixing old mistakes or making small repayments—you open yourself up to better financial opportunities.

And remember: improving your credit score isn’t about chasing a number. It’s about building a profile that tells the financial system—you can be trusted.

FAQs

1. How often does CIBIL update my score?

Typically, your score is updated every 30–45 days based on new data from lenders.

2. Will closing an old credit card hurt my score?

Yes. Older accounts help build your credit history. Closing them can shorten your credit age and slightly reduce your score.

3. Can I have a CIBIL score without taking a loan or credit card?

No. Your score is based on your credit history. If you’ve never taken credit, you won’t have a score—just a ‘NA’ or ‘NH’ report.

4. Is checking my CIBIL score often a bad thing?

No. Soft inquiries (when you check your score) have no impact on your credit score.

5. What’s the best way to start building credit from scratch in 2025?

Apply for a secured credit card or take a small loan via a regulated NBFC. Pay on time and track your report monthly.

Leave a Reply