You don’t have to look far to see the problem. The minute your house starts earning rental income, it starts attracting tax. It doesn’t matter whether it’s a small flat in Noida or a commercial shop in Pune — if it earns rent, the government wants a cut.

But here’s the good part.

Rental income may be taxable, but it also opens up legitimate tax-saving opportunities. No complex tricks. No black money. Just good old provisions under the Income Tax Act — quietly waiting to be used. The catch? Most people don’t even know they exist.

So let’s break it down — how to legally reduce the tax on your rental income in 2025 without getting caught in red tape.

- 1. Use the 30% Standard Deduction

- 2. Deduct Home Loan Interest (Unlimited for Rented Properties)

- 3. Deduct Municipal Taxes — But Only If You Pay Them

- 4. Let Joint Ownership Work in Your Favour

- 5. Claim Deduction on Unrealized Rent (If Tenant Defaults)

- 6. Opt for the Old Regime — In Most Cases

- 7. Renting to a Business? TDS Comes into Play

- 8. Consider HUF or Family Trust Ownership (Advanced Planning)

- ✅ Quick Recap — Smart Ways to Save Tax on Rental Income

- FAQs

- Conclusion: Pay Tax, But Pay Less

1. Use the 30% Standard Deduction

This is your first and most powerful tool. The Income Tax Act allows a flat 30% deduction on your Net Annual Value (NAV) under Section 24(a).

Let’s say your house earns ₹6,00,000 annually in rent. You paid ₹50,000 in municipal taxes. That leaves ₹5,50,000 as your NAV. On this, you immediately get a ₹1,65,000 deduction — no bills, no questions.

That’s how it works:

- Gross Annual Rent: ₹6,00,000

- Less: Municipal Taxes: ₹50,000

- Net Annual Value (NAV): ₹5,50,000

- Less: 30% Standard Deduction: ₹1,65,000

- Taxable Rental Income: ₹3,85,000

That’s real savings — clean, automatic, and fully legal.

2. Deduct Home Loan Interest (Unlimited for Rented Properties)

Here’s where things get even more interesting.

If you’ve taken a home loan for the rented property, the interest you pay is deductible under Section 24(b). And unlike self-occupied houses (where the limit is ₹2,00,000), rented-out properties have no upper limit.

So even if your interest payout is ₹6,00,000 for the year — you can claim the full amount as a deduction.

Example:

- Annual Rental Income (NAV): ₹5,50,000

- Standard Deduction (30%): ₹1,65,000

- Interest on Home Loan: ₹6,00,000

Net Taxable Rental Income = Negative. This loss can offset other income heads like salary or capital gains — resulting in even more savings.

3. Deduct Municipal Taxes — But Only If You Pay Them

A common mistake people make? Forgetting to deduct municipal or property taxes.

If you, the owner, pay them during the year, you can subtract the full amount from your gross rental income before applying the 30% deduction.

But remember — the timing matters. You can only claim what you’ve actually paid in that financial year.

note:-

4. Let Joint Ownership Work in Your Favour

Say a husband and wife co-own a property. The rental income doesn’t belong to one person — it gets split in the ratio of ownership.

This matters because if one spouse is in the 30% tax slab and the other has no income, you’ve just sliced your total tax bill in half.

Let’s say:

- Property earns ₹8,00,000 annually

- Ownership: 50-50

- Spouse 1 has other income; Spouse 2 has none

In this case, ₹4,00,000 falls under each person. The second spouse may pay zero tax if their total income remains under the basic exemption.

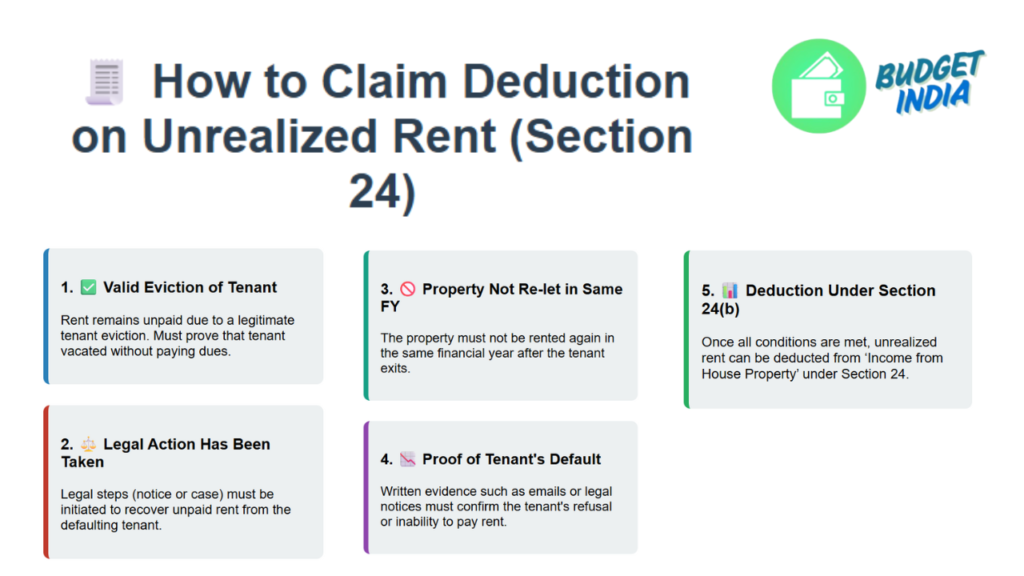

5. Claim Deduction on Unrealized Rent (If Tenant Defaults)

Life isn’t perfect. Tenants sometimes don’t pay up.

But under Rule 4 of the Income Tax Rules, if you tried to recover the rent through legal means and failed, you can claim a deduction for unrealized rent. This means the defaulted amount won’t be taxed in your hands.

Caveat: This only works if:

- Lease terms are documented

- Tenant has vacated or legal recovery has been initiated

- The amount is genuinely unrecoverable

So document everything. Without proof, it doesn’t fly.

6. Opt for the Old Regime — In Most Cases

In 2025, taxpayers still have to choose between:

- Old Tax Regime: Higher slabs, but allows all deductions

- New Tax Regime: Lower slabs, but no deductions

Now here’s the key: if your income includes rent, the old regime is usually more favourable — because it allows you to:

- Deduct interest on housing loan

- Use the 30% standard deduction

- Deduct municipal taxes

- Set off losses from property against other income

The new regime wipes all that out. So unless your rental income is small and your salary is huge, old regime is your better bet.

7. Renting to a Business? TDS Comes into Play

If your tenant is a company, firm or LLP, and the monthly rent exceeds ₹50,000, they’re required to deduct TDS at 10% before paying you.

Good news? This TDS is adjustable against your total tax liability. It’s not a separate tax — it’s just advance payment.

But make sure:

- You collect Form 16A from the tenant

- Declare the TDS in your ITR

- Match it with Form 26AS on the tax portal

8. Consider HUF or Family Trust Ownership (Advanced Planning)

For those with high-value property portfolios, consider transferring the asset to a HUF (Hindu Undivided Family) or a family trust. These structures are taxed separately from individuals and can significantly reduce the tax liability by spreading income.

But a word of caution — this is long-term tax planning, not short-term escape. Always consult a tax advisor before restructuring ownership.

✅ Quick Recap — Smart Ways to Save Tax on Rental Income

| Strategy | Benefit |

|---|---|

| 30% Standard Deduction | Automatic, no receipts needed |

| Interest on Home Loan (Sec 24b) | Unlimited for let-out property |

| Municipal Tax Paid | Fully deductible before standard deduction |

| Co-ownership | Splits income; reduces slab exposure |

| Unrealized Rent Deduction | Remove defaulted rent from tax liability |

| Old Tax Regime | Allows all deductions; best for property owners |

| HUF/Trust Setup | Advanced income structuring |

FAQs

Q1. Is rental income taxable under the new tax regime?

Yes, rental income is taxable under both regimes. But in the new regime, you lose out on most deductions like home loan interest and standard deduction.

Q2. What if I have more than one rented property?

Each property is assessed separately. Deductions apply individually — and if one property generates a loss, it can offset income from another.

Q3. Can I deduct maintenance charges paid to society?

No. Only municipal taxes and loan interest are allowed. Society charges, maintenance, or brokerage are not deductible under Section 24.

Q4. What if I receive rent in cash?

You must declare all rent, regardless of the mode of payment. Evading rent income is tax evasion — and penalties apply.

Q5. Can I set off rental income loss against salary income?

Yes. Under the old regime, losses from house property (mainly due to interest deduction) can be set off against salary or business income up to ₹2,00,000 per year.

Q6. Do I have to register the rent agreement?

Legally, yes — if the lease is over 11 months. While not mandatory for tax purposes, a registered agreement strengthens your claim on deductions like unrealized rent.

Conclusion: Pay Tax, But Pay Less

Owning property is a solid long-term play. But rental income, while steady, becomes a liability if you’re not optimizing it for tax. And unlike salary, where deductions are limited, rental income comes with a generous toolkit — if you know how to use it.

So whether you’ve rented out a flat in Bangalore or a commercial shop in Indore — the goal is simple:

Follow the rules. Claim what’s yours. Pay only what you owe. Nothing more.

Leave a Reply