Securing funding remains one of the most pressing challenges for Indian entrepreneurs—especially for those without assets to pledge. But here’s the good news: India’s lending ecosystem is evolving fast. Thanks to digital innovation, fintech disruption, and government-backed schemes, you can now access business loans without offering any collateral.

This 2025 guide walks you through everything you need to know about obtaining unsecured business loans in India. From eligibility and documents to lenders and smart borrowing strategies—we’ve covered it all. Whether you’re a startup founder, small business owner, or self-employed professional, this guide is your roadmap to financing growth without risking your personal or business assets.

Why Opt for an Unsecured Business Loan?

Unsecured loans are growing in popularity—and for good reason. Unlike traditional loans that require land, property, or machinery as security, unsecured business loans are primarily backed by your creditworthiness and cash flow.

Here’s why more entrepreneurs are going collateral-free:

- Asset Protection: You don’t have to risk personal or business assets.

- Faster Approvals: Digital lenders can disburse funds within 24–72 hours.

- Flexible Use: Spend the loan on working capital, expansion, inventory, or equipment.

- Credit Building: Timely repayments improve your CIBIL score.

- Government Support: Programs like MUDRA and CGTMSE make loans more affordable and accessible.

Step-by-Step Guide to Getting a Collateral-Free Business Loan

Step 1: Define the Purpose of the Loan

Before applying, know why you need funding and how you’ll use it. Lenders prefer borrowers who are financially disciplined and strategic.

Popular loan purposes include:

- Working capital for day-to-day operations

- Business expansion or new store launches

- Machinery, vehicle, or tech purchases

- Seasonal inventory stocking

- Consolidation of high-interest debts

Pro Tip: Build a solid business plan that demonstrates how the loan will generate returns. It not only increases your chances of approval but also helps you estimate the ideal loan amount.

Step 2: Check Your Credit Score (Aim for CIBIL 650+)

Your CIBIL score, ranging from 300 to 900, is the single most important factor for unsecured loans.

Credit Score Tiers:

- 750 & above: Eligible for the best rates

- 650–749: Acceptable, with slightly higher interest

- Below 650: Limited options, but fintech lenders may still consider your application

Improve Your Score By:

- Clearing outstanding credit card dues

- Keeping utilization below 30% of your limit

- Avoiding frequent loan applications

- Correcting inaccuracies on your credit report

Tip: If your score is low, consider taking a small secured credit product to rebuild your profile.

Step 3: Prepare the Required Documents

Here’s a list of common documents you’ll need for a seamless loan application:

Mandatory:

- PAN (business and personal)

- Aadhaar card

- Proof of business registration (GST, MSME/Udyam Certificate)

- Bank statements (last 6–12 months)

- ITRs (last 2–3 years)

Optional (but recommended):

- Projected financial statements (for new businesses)

- Details of existing loans, if any

- KYC of co-founders/partners

Note: Fintech lenders typically require fewer documents and offer faster processing.

Step 4: Compare Lenders and Schemes

Not all lenders are equal—compare offerings before you commit.

| Lender Type | Examples | Loan Amount | Interest Rate | Ideal For |

|---|---|---|---|---|

| Banks | SBI, HDFC, ICICI | ₹5L–₹2Cr | 10–18% | Established businesses |

| NBFCs | Tata Capital, Bajaj Finserv | ₹50K–₹50L | 12–24% | Businesses needing moderate sums |

| Fintechs | Lendingkart, KreditBee | ₹50K–₹30L | 15–30% | Startups & quick approvals |

| Govt. Schemes | MUDRA, CGTMSE, Stand-Up India | Up to ₹2Cr | 7–12% | Small and underserved businesses |

Compare interest rates, fees, repayment flexibility, and customer support before choosing your lender.

Step 5: Apply Online (Fastest Route)

How to Apply:

- Bank websites: More paperwork, longer turnaround

- Fintech apps: Paperless, fast-track approvals

- Govt. Portals: Udyam or SIDBI platforms for schemes like MUDRA

Typical Timelines:

- Fintech: 24–48 hours

- NBFCs/Banks: 3–7 days

- Govt. Schemes: 1–2 weeks

Tip: Ensure your application is accurate to avoid delays or rejections.

Step 6: Review the Terms Before Signing

Before accepting any offer, take a moment to carefully read the fine print.

Check for:

- Fixed vs floating interest rate

- Processing and late payment fees

- Prepayment penalties

- EMI affordability (use calculators)

- Default consequences and legal terms

Tip: Negotiate better terms if your business has strong cash flow or you’re an existing customer.

Step 7: Disbursement and Responsible Repayment

Once funds are credited, the real work begins.

Smart Post-Loan Habits:

- Spend only on intended business activities

- Keep records of all loan-related transactions

- Set up auto-debit for EMI payments

- Monitor cash flow to avoid missed payments

Avoid These Pitfalls:

- Diverting funds to personal use

- Taking additional loans without capacity

- Missing EMIs, which damages your credit history

Make partial prepayments when possible to reduce interest burden.

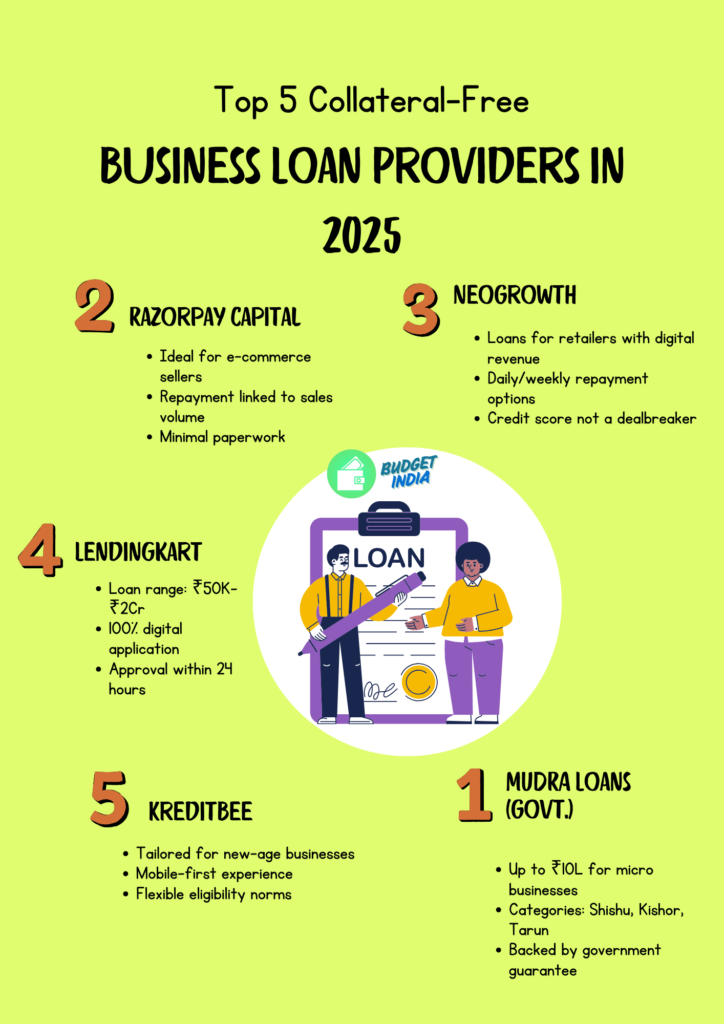

Top 5 Collateral-Free Business Loan Providers in 2025

Here’s a quick roundup of top lenders offering unsecured loans this year:

- Lendingkart

- Loan range: ₹50K–₹2Cr

- 100% digital application

- Approval within 24 hours

- Razorpay Capital

- Ideal for e-commerce sellers

- Repayment linked to sales volume

- Minimal paperwork

- NeoGrowth

- Loans for retailers with digital revenue

- Daily/weekly repayment options

- Credit score not a dealbreaker

- MUDRA Loans (Govt.)

- Up to ₹10L for micro businesses

- Categories: Shishu, Kishor, Tarun

- Backed by government guarantee

- KreditBee

- Tailored for new-age businesses

- Mobile-first experience

- Flexible eligibility norms

FAQs: Unsecured Business Loans in India

1. Can I get a business loan without collateral in 2025?

Absolutely. Banks, NBFCs, fintech platforms, and government schemes offer unsecured loans based on credit history and cash flow.

2. What CIBIL score is required?

A score above 650 is preferred. Some fintechs may consider scores as low as 550 with strong revenue proof.

3. How soon can I get the funds?

Fintechs disburse within 48 hours, banks in 3–7 days, and government schemes may take 1–2 weeks.

4. What if I have a low credit score?

Try these:

- Add a co-applicant

- Offer alternate collateral like FD or insurance

- Apply via fintechs that use alternate credit models

- Improve score and reapply in 3–6 months

5. Are MUDRA loans really collateral-free?

Yes. MUDRA loans under the PMMY scheme are designed to support small and micro enterprises without asking for collateral.

Final Recommendations

- Build Your Credit: Aim for a score of 750+ to unlock premium offers

- Explore Subsidized Loans: Don’t overlook MUDRA, CGTMSE, or SIDBI options

- Use Comparison Tools: Check rates, terms, and reviews before choosing a lender

- Stay Financially Disciplined: Timely repayments secure future funding

- Get Professional Advice: A CA can help optimize loan structure and tax benefits

India’s credit ecosystem in 2025 is more inclusive than ever. With the right strategy and financial discipline, you can secure the funds to scale your business—no collateral needed.

Need help selecting the right loan? Speak to your banker, financial advisor, or explore trusted online aggregators to get started.

Leave a Reply