UPI Credit Line Explained: How It Works, Who Can Use It, and Why It Matters in 2025

A quick easy breakdown of RBI’s new UPI-based credit line system—what it means for banks, users, and India’s digital economy

Since the launch of UPI (India’s Unified Payments Interface) by Dr. Raghuram G. Rajan, the then Governor of RBI, in Mumbai. It became a revolution, transforming how millions transact daily. By completely changing the landscape of digital payment in India.From street vendors to online shoppers, the Unified Payments Interface (UPI) has become the undisputed king, a testament to its simplicity and efficiency. But what if this powerhouse could do more than just facilitate payments? What if it could also offer you instant access to credit, seamlessly integrated into your daily digital life? Well the all these question are now been answer by the The Reserve Bank of India (RBI) who now wants to make credit simpler, faster, and more accessible — especially for those who’ve been historically left out of formal credit channels.

Thus they introduction UPI Credit Line a a financial innovation poised to redefine personal borrowing and digital convenience.

And if UPI transformed how India pays, UPI Credit Line could soon transform how India borrows.

It’s already live. Some of the biggest banks have rolled it out. And it works on the same UPI apps you already use — no new cards, no paperwork, and no middlemen.

But how does it work? Who can use it? And is it better than credit cards? This guide breaks down everything you need to know.

What is a UPI credit line?

An NBFC or bank gives you a UPI credit line, which is a pre-approved credit amount that is linked directly to your UPI ID. Now, instead of spending your own money, you can make purchases on UPI ID and pay back later—just like a credit card, but without the physical plastic.

In simple terms, instead of using your own money via UPI, now you can use borrowed money directly through your UPI apps. That’s the UPI Credit Line.

Now I know some of you are thinking about the interest.

So, don’t worry about the interest; it is only levied on the precise amount you utilize for your payments. That is what makes it an incredibly efficient and cost-effective borrowing solution. It’s a fundamental shift from traditional credit, embracing the agility and immediacy that digital finance promises.

Key Features That Make UPI Credit Line Stand Out

The UPI Credit Line isn’t just a new product; it’s a suite of features designed for the modern digital consumer:

- Pre-Approved Credit Limits: Based on your financial profile and the issuing bank’s assessment, you receive a predetermined credit limit, ready for immediate use.

- Easy Setup: The entire activation process is digital, typically completed within your existing UPI-enabled banking or payment app.

- Real-Time Tracking: Keep a close eye on your usage, outstanding balance, and available credit, all updated in real-time within your app.

- Flexible Repayment Options: Pay back your utilized amount at your convenience, adhering to the terms set by the issuing bank, often with options for minimum payments or full settlements.

Advantages: Why UPI Credit Line is a Game-Changer for Digital Transactions

The strategic brilliance here is multifold. The UPI Credit Line isn’t just about offering another credit option; it’s about optimizing the borrowing experience for the digital age:

- Instant Access to Credit: Need funds immediately for an unexpected expense or a timely purchase? The UPI Credit Line delivers.

- Flexible and Potentially Lower Borrowing Costs: By charging interest only on the amount you actually use, it can be more economical than carrying a balance on a traditional credit card.

- No Physical Card Required: Embracing the true spirit of digital payments, there’s no plastic card to carry, lose, or forget. Your smartphone is your wallet and your credit line.

- Simplified Application and Approval: The digital process often means quicker approvals compared to the traditional paperwork-heavy procedures for credit cards or personal loans.

- Promotes Financial Inclusion: This innovation has the potential to bring millions more into the formal credit system, offering small, accessible credit to those who might otherwise struggle to obtain it.

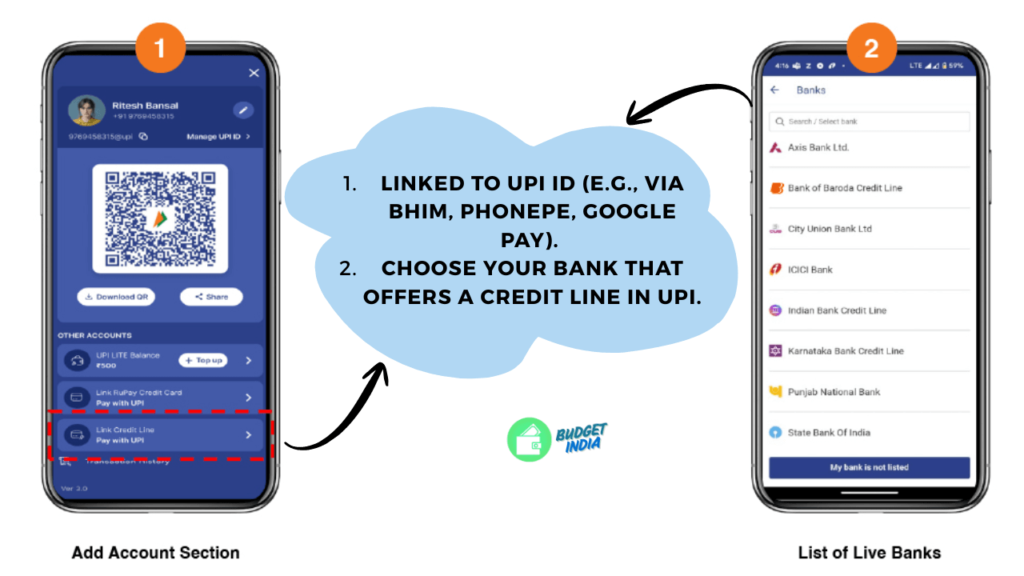

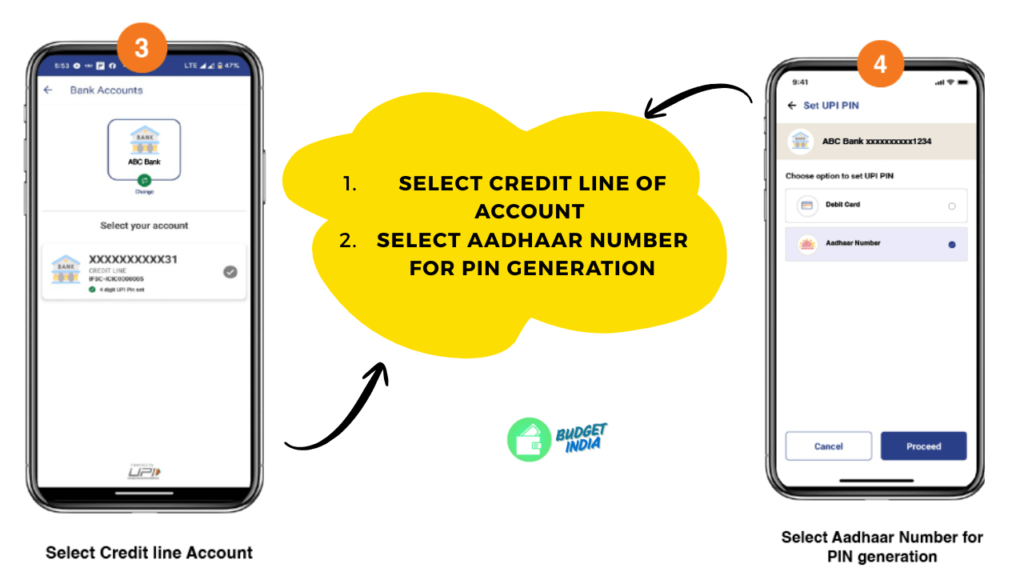

How Does the UPI Credit Line Work?

UPI Credit Line works through your existing UPI apps like PhonePe, Paytm, and Google Pay.

Here’s how it works:

- Your bank approves a credit limit—let’s say ₹50,000.

- You go to a merchant or pay someone using UPI.

- Instead of selecting your bank account, you choose the credit line option.

- The money is debited from your approved limit.

- You repay later, either in full or through EMIs (depending on the terms).

Easy peasy Isn’t it? You only pay interest on what you use. And the rest of the limit stays intact.

Why Is RBI Pushing UPI Credit Lines Now?

I know, we are all still thinking about why this new credit is needed and why RBI wants to push this thing.

The answer you might know,

Let’s be honest—credit cards never scaled beyond urban India.

Even today, fewer than 5% of Indians own a credit card. That’s a massive credit gap. But what everyone does have is UPI.

So the logic is simple—if people already use UPI for spending, why not let them borrow directly through the same system?

It helps the RBI:

- Expand formal credit access

- Reduce dependency on physical cards and POS machines

- Enable small-ticket digital lending at scale

It’s financial inclusion without friction.

UPI Credit Line vs Credit Card: What’s the Difference?

On the surface, both let you spend on credit. But scratch a little deeper and you’ll see some key differences:

| Feature | Credit Card | UPI Credit Line |

| Access Method | Card / Virtual Card | UPI QR or UPI ID |

| Interest-free period | Up to 45 days | Varies (bank-defined) |

| Fees & Charges | Annual charges apply | Likely zero or minimal |

| Acceptance | POS/Online only | Any UPI-enabled merchant |

| Credit Limit | Varies, harder to get | More inclusive |

Who Can Use UPI Credit Line Right Now?

Currently, the facility is being offered by:

- State Bank of India (SBI)

- HDFC Bank

- Punjab National Bank (PNB)

- Axis Bank

- ICICI Bank

- Bank of Baroda and others

However, it’s not available to everyone yet.

Banks are selectively offering it to existing customers who meet their creditworthiness criteria. So if you don’t see the option on your UPI app yet, it just means your bank hasn’t activated it for you.

Who Can Get a UPI Credit Line? Eligibility Criteria

The process for obtaining a UPI Credit Line is intended to be simple:

- Generally speaking, applicants must be at least eighteen years old.

- Active Savings Account: A bank that offers UPI Credit Lines and supports the service must have an active savings account.

- Activated UPI Account: It goes without saying that you need to have your UPI account created and operational.

While these are the basic requirements, the issuing banks will conduct their own credit assessment to determine your eligibility and the credit limit. This typically involves checking your credit history and financial standing.

Our Opinion

Just like BHIM and Paytm made payments democratic, the UPI Credit Line could do the same for credit.

It’s still early days, but the direction is clear — India is moving toward a credit system that’s fully digital, deeply integrated, and radically simple.

And in that future, you may never need a credit card at all.

Well, that’s it for now.

If you found this article helpful, please do share it with your friends and family.

Also, drop a comment below and tell us — what’s your take on the UPI Credit Line?

What’s your valuable point of view on this new move by RBI? We’d love to hear it.

Leave a Reply