Investing or dealing with property in India involves several important tax considerations. The two primary taxes that property owners must be aware of are Property Tax and Capital Gains Tax. These taxes differ in purpose, calculation methods, and timing of payment. This article explains the essentials of Property Tax, details how Capital Gains Tax on property sales is computed, outlines available reliefs, and presents the latest updates effective from 2025.

- 1. Distinguishing Property Tax from Capital Gains Tax

- 2. Key Points on Capital Gains Tax for Property

- 3. Calculating Capital Gains Tax

- 4. Methods to Minimize Capital Gains Tax Liability

- 5. Important Records to Maintain

- 6. 2025 Budget Updates Affecting Property and Capital Gains Tax

- 7. Practical Recommendations for Property Sellers

- Conclusion

- Frequently Asked Questions (FAQs)

1. Distinguishing Property Tax from Capital Gains Tax

1.1 Understanding Property Tax

Property Tax is a recurring charge levied by local authorities on property owners. The revenue generated helps fund public infrastructure and municipal services such as street maintenance, water supply, and sanitation systems.

- Collected annually based on property ownership

- Imposed by municipal corporations or local governing bodies

- Determined by property characteristics such as area, classification, and location

- Independent of property sale or ownership transfer

1.2 What is Capital Gains Tax?

Capital Gains Tax is a one-time tax levied on the profit earned when a property is sold.

- Payable only upon the sale of the property

- Calculated as the difference between the sale amount and the original purchase cost

- Administered by the Central Government’s Income Tax Department

- Applicable only if the sale yields a profit

1.3 Summary Table of Differences

| Aspect | Property Tax | Capital Gains Tax |

|---|---|---|

| Nature of Tax | Annual tax on property ownership | One-time tax on capital appreciation |

| Tax Authority | Local Municipal Corporation | Central Government (Income Tax Dept.) |

| Frequency | Every year | Upon property disposal |

| Purpose | Fund civic amenities | Tax on gains from property sale |

2. Key Points on Capital Gains Tax for Property

Capital Gains Tax applies only when the sale price exceeds the original purchase price. The tax rate varies depending on the duration for which the property was held.

2.1 Short-Term Capital Gains (STCG)

- Applicable if the property is sold within 24 months from the date of purchase

- Taxed as per the individual’s applicable income tax slab rates

- No allowance for inflation adjustment

2.2 Long-Term Capital Gains (LTCG)

- Applies when the property is held for more than 24 months

- Taxed at a fixed rate of 20%

- Eligible for indexation benefit to account for inflation

3. Calculating Capital Gains Tax

3.1 Short-Term Capital Gains Computation

This gain is added to the total income and taxed according to applicable slab rates.

3.2 Long-Term Capital Gains Computation

Where:

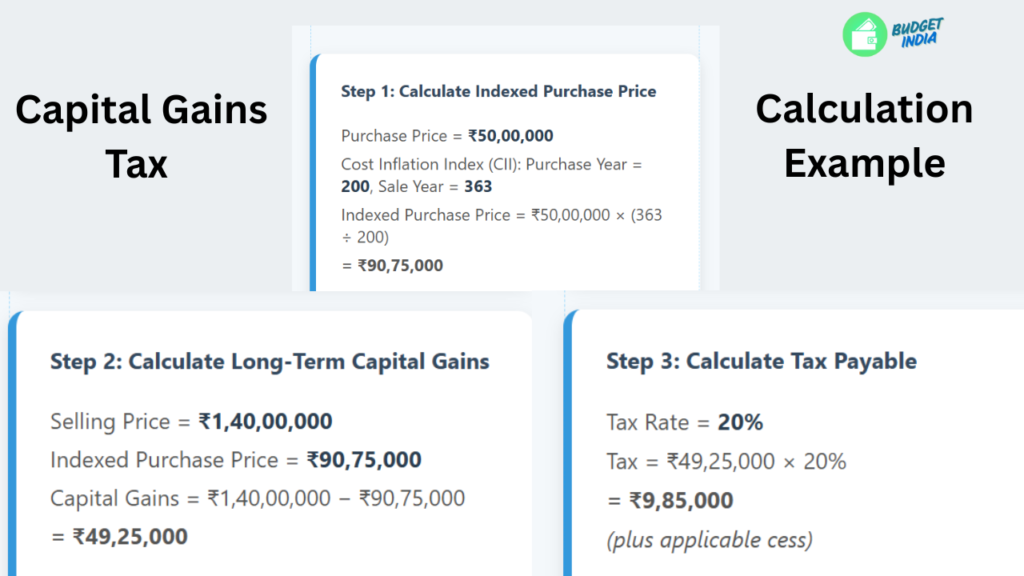

Example for a Property Sold in 2025:

| Description | Value |

| Purchase Price (2012) | ₹50,00,000 |

| Sale Price (2025) | ₹1,40,00,000 |

| Cost Inflation Index (2012-13) | 200 |

| Cost Inflation Index (2025-26) | 363 |

Indexed Purchase Price = ₹50,00,000 × (363 / 200) = ₹90,75,000

Capital Gains = ₹1,40,00,000 – ₹90,75,000 = ₹49,25,000

Tax @ 20% = ₹9,85,000 (plus applicable cess)

4. Methods to Minimize Capital Gains Tax Liability

4.1 Section 54 – Reinvestment in Residential Property

Tax relief is available if the capital gains are reinvested in purchasing a new residential house within two years or constructing one within three years of the sale.

4.2 Section 54EC – Investment in Specified Government Bonds

Investments up to ₹50 lakh in bonds issued by bodies such as NHAI or REC made within six months of the sale are exempt from capital gains tax. The bonds must be held for a minimum of five years.

4.3 Section 54F – Reinvestment from Sale of Non-Residential Property

To claim exemption, the entire sale proceeds from a non-residential property must be reinvested in a residential property.

5. Important Records to Maintain

To facilitate tax filing and exemption claims, it is essential to keep:

- Sale and purchase agreements

- Receipts for renovations or capital improvements

- Bills for brokerage, legal fees, and transfer costs

- Proof of new property purchase or government bond investments

- Property tax payment receipts as ownership evidence

6. 2025 Budget Updates Affecting Property and Capital Gains Tax

- LTCG surcharge limited to 15%, lowering tax burden

- Mandatory linking of PAN and Aadhaar for exemption claims

- Sharing of municipal property valuations with Income Tax authorities

- Deployment of AI systems to monitor high-value real estate transactions for compliance

7. Practical Recommendations for Property Sellers

- Retaining property for over two years qualifies for LTCG tax benefits and indexation

- Maintain thorough documentation of all expenses and taxes paid

- Timely reinvestment of gains is critical to maximize tax exemptions

- Consult a tax advisor prior to sale to optimize tax outcomes

Conclusion

A clear comprehension of property taxation, especially Capital Gains Tax, is crucial for property owners and investors in India. With property prices rising and compliance requirements tightening in 2025, proactive tax planning and proper record maintenance can substantially reduce tax liabilities. Professional guidance can further help optimize tax savings and ensure adherence to regulations.

Frequently Asked Questions (FAQs)

Q1: Does Capital Gains Tax apply to inherited property?

You are liable to pay Capital Gains Tax only when you sell the inherited property. For tax purposes, you must consider the acquisition date and cost of the original owner.

Q2: Is agricultural land exempt from Capital Gains Tax?

Rural agricultural land as defined under the Income Tax Act is exempt, but agricultural land located in urban areas is taxable.

Q3: Can Non-Resident Indians (NRIs) claim Capital Gains exemptions in India?

Yes, NRIs are eligible for exemptions under Sections 54 and 54EC if the stipulated conditions are fulfilled.

Q4: Are repayments of home loans deductible from Capital Gains?

No, home loan repayments do not reduce capital gains. Only expenses related to renovation or improvement are deductible.

Leave a Reply